Your credit score plays a major role in your financial life. Whether you want to apply for a credit card buy a car get a personal loan or qualify for a mortgage lenders use your credit score to evaluate how financially responsible you are. That’s why understanding how to improve credit score is one of the smartest financial moves you can make.

A good credit score can help you secure lower interest rates faster loan approvals and better financial opportunities. On the other hand a poor score may lead to loan rejections higher borrowing costs and financial stress.

The good news is that improving your credit score is possible for almost everyone. It does not happen overnight but with consistent habits and smart financial decisions you can gradually build a stronger credit profile.

In this detailed guide by FinoraLab you will learn what a credit score is how it works what affects it and practical strategies you can use to improve your score in a realistic and sustainable way.

Key Takeaways

Your credit score reflects your creditworthiness and financial behavior.

Paying bills on time is one of the most important factors in improving your score.

Keeping credit card balances low can significantly help your credit utilization ratio.

Checking your credit report regularly helps identify errors and fraud.

Avoiding unnecessary loan applications can protect your score from hard inquiries.

Long-term consistency matters more than quick fixes.

What Is a Credit Score?

A credit score is a three-digit number that represents how likely you are to repay borrowed money responsibly. Financial institutions such as banks lenders and credit card companies use this score to assess risk before approving loans or credit applications.

Most credit scoring systems range between 300 and 850.

Credit Score Range

Rating

300–579

Poor

580–669

Fair

670–739

Good

740–799

Very Good

800–850

Excellent

A higher score generally means you are considered a lower-risk borrower.

Why Credit Scores Matter in Modern Finance

In today’s financial system credit scores affect far more than just loans. Many landlords insurance companies and even employers may review your credit history in certain situations.

Here are some real-world areas where your credit score matters:

Mortgage approvals

Car financing

Credit card eligibility

Personal loans

Business financing

Apartment rentals

Insurance premiums

For example two people applying for the same car loan may receive completely different interest rates based on their credit scores. A borrower with excellent credit could save thousands of dollars in interest over time compared to someone with poor credit.

How Credit Scores Are Calculated

Credit scoring models consider several factors from your credit history. Although the exact formulas vary most scoring systems use similar categories.

Payment History

Payment history is usually the largest factor affecting your score. Lenders want to know whether you pay your bills on time.

Late payments defaults collections and bankruptcies can seriously damage your score.

Credit Utilization Ratio

This measures how much of your available credit you are currently using.

For example if your credit card limit is $10000 and your current balance is $2000 your utilization ratio is 20%.

Experts generally recommend keeping utilization below 30% although lower is even better.

Length of Credit History

Older credit accounts can positively impact your score because they demonstrate long-term financial responsibility.

Credit Mix

Having a mix of different credit types such as credit cards auto loans and installment loans may slightly improve your score.

New Credit Inquiries

Applying for multiple loans or credit cards within a short period can lower your score temporarily because lenders may view it as risky behavior.

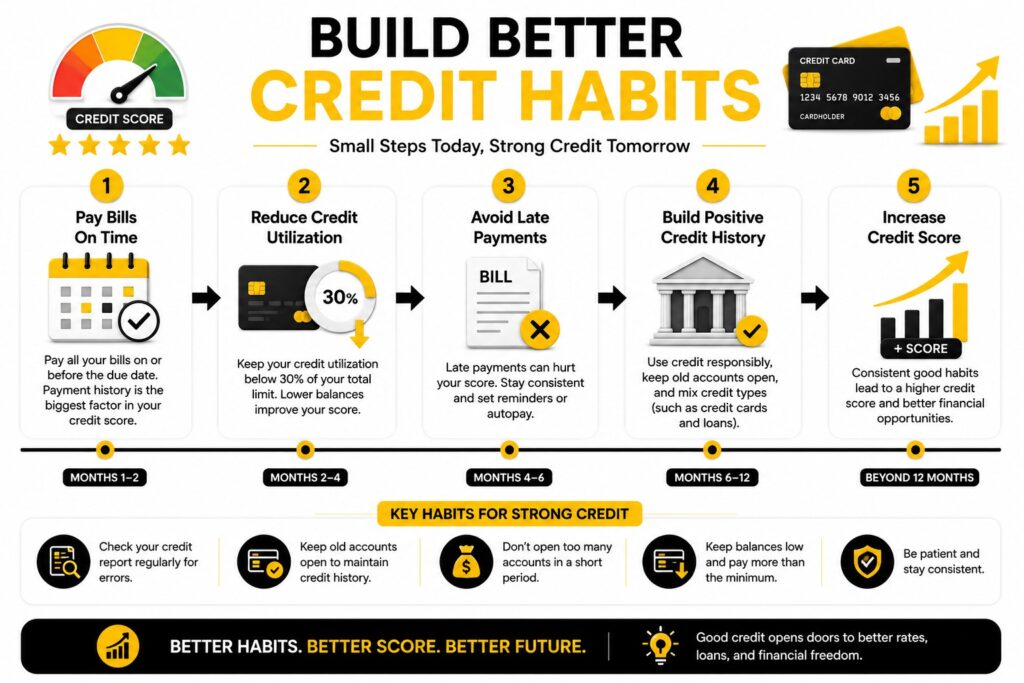

How to Improve Credit Score Effectively

Improving your credit score requires patience and consistency. Below are the most effective strategies that actually work in real life.

Pay All Bills on Time

Your payment history is the foundation of your credit score.

Even one missed payment can negatively impact your profile for years. Set reminders automate payments or use banking apps to ensure bills are paid before the due date.

This includes:

Credit cards

Utility bills

Personal loans

Student loans

Mortgage payments

Many people underestimate how quickly late payments can damage their credit.

Real-World Example

Imagine two borrowers:

Sarah pays every bill on time for five years.

John misses multiple payments during the same period.

Even if both earn similar incomes Sarah will likely qualify for lower-interest loans and better financial opportunities.

Keep Credit Card Balances Low

A common mistake people make is maxing out their credit cards.

High balances increase your credit utilization ratio which signals potential financial stress to lenders.

If possible:

Keep utilization below 30%

Aim for below 10% for excellent scores

Pay balances multiple times per month

Example Calculation

Suppose you have:

Credit Card Limit: $5000

Current Balance: $4000

Your utilization ratio would be:

\frac{4000}{5000} \times 100 = 80%

An 80% utilization ratio is considered very high and can hurt your score significantly.

Avoid Applying for Too Much Credit

Every time you apply for a loan or credit card a hard inquiry may appear on your report.

One inquiry is usually not a major issue. However multiple applications in a short period may lower your score and make lenders nervous.

Before applying for new credit:

Compare offers carefully

Apply only when necessary

Avoid opening multiple cards at once

Check Your Credit Report Regularly

Many people never review their credit reports which is risky.

Errors can occur due to:

Incorrect balances

Fraudulent accounts

Identity theft

Reporting mistakes

Regularly checking your report helps you catch problems early.

If you find inaccuracies dispute them immediately with the credit bureau.

Keep Old Credit Accounts Open

Closing old accounts may seem like a good idea but it can actually reduce your average credit age and increase utilization ratios.

For example:

If you close a card with a high credit limit your total available credit decreases. This can make your utilization ratio look worse even if your spending stays the same.

Unless there are annual fees or serious issues keeping older accounts open often benefits your score.

Diversify Your Credit Mix Carefully

Lenders like to see responsible handling of different credit types.

A healthy credit mix may include:

Credit cards

Auto loans

Personal loans

Mortgages

However never borrow money unnecessarily just to improve your score.

The goal is responsible credit management not accumulating debt.

Negotiate Outstanding Debts

If you have overdue accounts or collections ignoring them rarely helps.

Instead:

Contact creditors directly

Negotiate payment plans

Request settlement agreements

Ask for goodwill adjustments if appropriate

Many lenders are willing to work with borrowers who communicate honestly.

Become an Authorized User

A lesser-known strategy is becoming an authorized user on someone else’s well-managed credit card.

If the primary cardholder has:

Excellent payment history

Low utilization

Long account age

Their positive credit behavior may help your score as well.

However choose carefully because negative activity can also affect you.

Use Secured Credit Cards Wisely

For beginners or individuals rebuilding poor credit secured credit cards can be useful tools.

A secured card requires a refundable security deposit which acts as collateral.

Responsible use can gradually build positive credit history.

Common Mistakes That Hurt Credit Scores

Many people unknowingly damage their scores through avoidable mistakes.

Missing Payments

Even small late payments can stay on reports for years.

Maxing Out Credit Cards

High balances increase utilization ratios dramatically.

Closing Old Accounts

This can shorten your credit history and increase utilization.

Applying for Too Many Loans

Frequent inquiries may signal financial instability.

Ignoring Credit Reports

Unnoticed errors or fraud can quietly damage your score.

How Long Does It Take to Improve a Credit Score?

One of the most common questions people ask is how quickly credit scores improve.

The answer depends on your financial situation and past history.

Minor Issues

If your score dropped due to high utilization paying balances down could improve it within a few months.

Serious Negative Marks

Bankruptcies defaults and collections may take years to recover from fully.

Generally meaningful improvement often takes:

3–6 months for minor improvements

1–2 years for stronger rebuilding

Longer for severe credit damage

Consistency is the key factor.

Credit Scores and Loan Interest Rates

A higher credit score can save you substantial money through lower interest rates.

Loan payments are often calculated using compound interest principles.

In some industries financial trustworthiness directly affects business opportunities.

Building Credit From Scratch

Young adults and first-time borrowers often struggle because they have little or no credit history.

Some beginner-friendly strategies include:

Starting with a secured credit card

Becoming an authorized user

Using student credit cards responsibly

Making small purchases and paying balances in full

Building strong credit early creates long-term financial advantages.

Can You Improve Your Credit Score Fast?

There are no guaranteed overnight fixes.

Be cautious of companies promising “instant credit repair” because many use misleading tactics.

However some actions may create faster improvements:

Paying down high balances

Correcting report errors

Catching up on missed payments

Requesting credit limit increases responsibly

Real credit improvement is usually gradual and based on consistent habits.

Psychological Habits Behind Good Credit

Interestingly strong credit scores are often connected to broader financial behaviors.

People with healthy credit habits usually:

Budget carefully

Avoid emotional spending

Maintain emergency savings

Plan purchases in advance

Track financial goals consistently

Improving your mindset around money can positively affect your score over time.

Credit Score Myths You Should Ignore

There are many misconceptions about credit scores online.

Myth: Checking Your Own Score Hurts Credit

False. Personal credit checks are usually soft inquiries and do not affect scores.

Myth: Carrying a Balance Improves Credit

False. Paying balances in full is generally better financially.

Myth: Income Directly Determines Credit Score

Income itself is not part of most scoring formulas.

Myth: Closing Cards Always Helps

Closing accounts can sometimes reduce scores instead.

Real-Life Scenario: Improving Credit Step by Step

Consider a person named Ahmed:

Credit Score: 560

Multiple late payments

High card balances

Ahmed starts improving his habits by:

Paying bills on time

Reducing utilization below 30%

Avoiding unnecessary loan applications

Monitoring his credit monthly

After 12 months his score improves to 690.

This improvement allows him to qualify for lower-interest financing and better financial opportunities.

Conclusion

Learning how to improve credit score is one of the most valuable financial skills you can develop. Your credit score affects borrowing costs loan approvals financial flexibility and even long-term wealth-building opportunities.

The process is not about quick tricks or shortcuts. Instead it involves building responsible habits over time. Paying bills consistently keeping balances low monitoring your credit report and avoiding unnecessary debt can gradually strengthen your financial profile.

Whether you are rebuilding damaged credit or starting from scratch small consistent improvements can make a major difference. The earlier you begin managing your credit responsibly the more financial opportunities you can unlock in the future.

At FinoraLab smart financial education starts with practical knowledge and realistic strategies. Improving your credit score is not just about numbers — it is about creating stronger financial stability and freedom for the future.

FAQs

How can I improve my credit score quickly?

The fastest ways include paying down high credit card balances correcting credit report errors and making all payments on time.

What is considered a good credit score?

A score above 670 is generally considered good while scores above 740 are viewed as very good or excellent.

Does checking my credit score lower it?

No. Personal credit checks are usually soft inquiries and do not affect your score.

How long do late payments stay on a credit report?

Late payments can remain on your credit report for up to seven years.

Is it better to pay off credit cards in full?

Yes. Paying balances in full helps reduce interest costs and keeps utilization low.

Can I improve my credit score without a credit card?

Yes. Loans rent reporting services and responsible payment history can also help build credit.

Why did my credit score drop after paying off a loan?

Sometimes paying off a loan changes your credit mix or reduces account history causing temporary score fluctuations.

How often should I check my credit report?

Checking your credit report at least once every few months is a smart financial habit

I am a professional finance content writer with expertise in personal finance investing, banking, loans, insurance, credit cards, budgeting, and market related topics. I create clear, SEO optimized, and reader friendly finance content that helps audiences understand complex financial concepts in simple words. My goal is to write trustworthy and engaging content that improves search visibility, builds credibility, and supports business growth.