Dave Ramsey Retirement Calculator: How It Works What It Gets Right and Whether You Should Trust the Numbers

Shanzay Arain·May 26, 2026

Retirement planning used to feel like something reserved for wealthy executives pension-backed workers or financial advisors managing million-dollar portfolios. Today it has become a mainstream financial survival strategy. Inflation rising healthcare costs unstable job markets and growing uncertainty around Social Security have pushed millions of Americans to search for smarter ways to calculate their future financial security. That is why the phrase “Dave Ramsey retirement calculator” has become one of the most searched retirement-related terms online.

People are not just looking for a calculator. They are looking for reassurance. They want to know whether they are saving enough whether retirement is even realistic anymore and how long it will take to build wealth that can sustain their lifestyle. In many cases users searching this keyword are emotionally overwhelmed. They may have debt inconsistent income streams or limited investing knowledge. Others are entrepreneurs creators freelancers or small business owners trying to replace traditional pensions with self-built retirement systems.

The popularity of the Dave Ramsey retirement calculator also reflects a major cultural shift in personal finance media. Financial personalities have become powerful digital brands. Dave Ramsey is not only a radio host and finance educator. He represents an entire business ecosystem built around budgeting psychology financial discipline debt elimination and long-term investing. His retirement calculator serves as both a practical financial tool and a gateway into a broader financial philosophy centered on behavioral money management.

At the same time retirement planning itself has evolved dramatically. Modern wealth building now includes creator economy income digital businesses real estate cash flow affiliate marketing YouTube monetization licensing income startup equity and fintech investments. Younger investors are no longer relying solely on employer-sponsored retirement accounts. They are building multi-income financial ecosystems designed to create flexibility passive income and long-term asset growth.

Understanding how the Dave Ramsey retirement calculator works requires more than simply plugging in numbers. It involves understanding the psychology behind retirement planning the assumptions used in financial projections and the real-world investing behaviors that determine whether people actually achieve financial independence. That deeper context is what makes this topic far more important than a simple online calculator review.

Why the Dave Ramsey Retirement Calculator Became So Popular

The rise of the Dave Ramsey retirement calculator is closely connected to how personal finance content changed over the past two decades. Traditional retirement planning once relied heavily on financial advisors complex spreadsheets and intimidating investment language. Dave Ramsey simplified the conversation. His brand transformed retirement planning into something emotionally understandable for middle-class families new investors and financially stressed households.

One reason the calculator became popular is because it aligns with behavioral finance principles rather than purely technical investing theory. Many people already know they should save for retirement. The bigger problem is consistency. Dave Ramsey’s financial ecosystem focuses heavily on habits discipline and psychological momentum. The calculator acts as a motivational tool by helping users visualize future wealth accumulation instead of viewing retirement as an abstract concept decades away.

The calculator also gained traction because of content marketing and digital media expansion. Financial personalities today function similarly to modern influencers. Dave Ramsey built a media empire through radio shows podcasts YouTube content books online courses and partnerships. His financial tools naturally became part of a broader creator economy strategy that monetizes audience trust while educating consumers. This approach mirrors how many modern finance creators build wealth today through digital products affiliate marketing sponsorships and educational subscriptions.

Another reason for its popularity is timing. Americans increasingly feel anxious about retirement. Pension systems have weakened inflation pressures continue rising and many workers lack confidence in Social Security sustainability. Financial calculators offer a sense of control during uncertain economic conditions. Users searching for the Dave Ramsey retirement calculator are often seeking clarity during moments of financial stress or life transition.

How the Dave Ramsey Retirement Calculator Actually Works

At its core the Dave Ramsey retirement calculator estimates how much wealth users could accumulate by retirement based on current savings monthly contributions expected investment returns and time horizon. The simplicity of the tool is one of its strongest advantages because it removes much of the technical intimidation that keeps people from engaging with retirement planning in the first place.

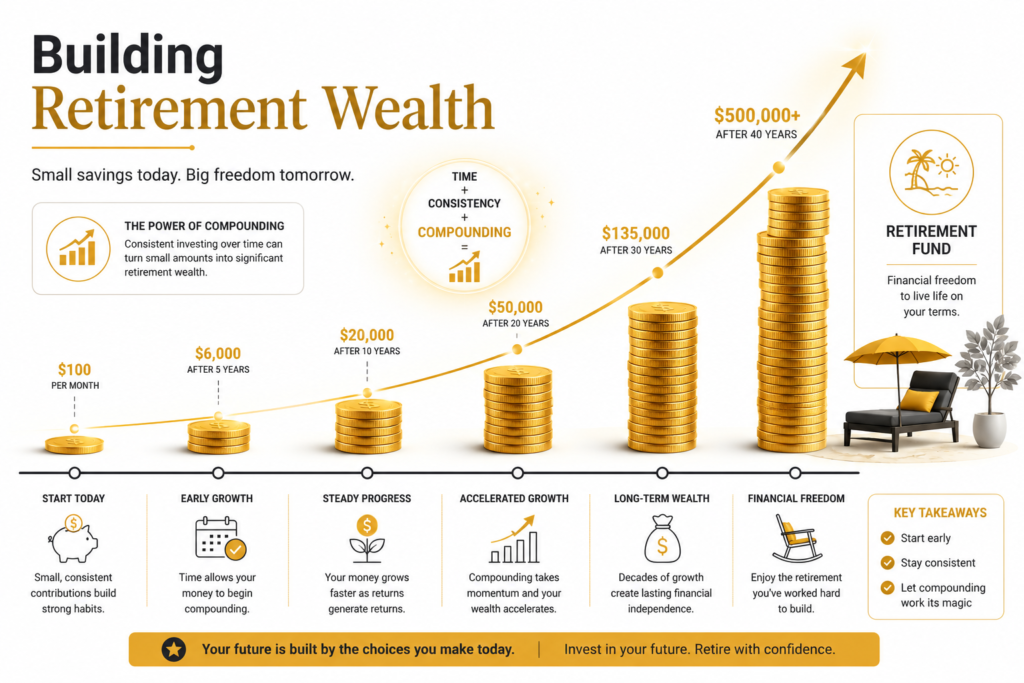

Typically users enter their current age retirement age goal annual income existing retirement savings and expected monthly investment contributions. The calculator then projects future portfolio growth using compound interest assumptions. Compound growth remains one of the most powerful concepts in finance because investment earnings themselves generate additional earnings over time.

One reason Dave Ramsey’s retirement philosophy resonates with many Americans is his aggressive optimism regarding long-term stock market returns. His projections often assume relatively strong annual market performance which can produce encouraging future balances. Critics argue these estimates may sometimes create overly optimistic expectations if users fail to account for inflation taxes or lower-than-expected returns during economic downturns.

Still the calculator succeeds in one important area: it motivates action. Financial planning tools are useless if people never use them. Ramsey’s platform simplifies investing concepts for average households that might otherwise avoid retirement planning entirely. Even conservative financial advisors acknowledge that getting people emotionally engaged with saving is often more important than perfect forecasting accuracy.

The broader lesson here extends into wealth psychology itself. Successful investing is rarely about mathematical perfection alone. It depends heavily on consistency emotional discipline and long-term thinking. Calculators can provide projections but financial behavior determines actual outcomes.

Understanding the Psychology Behind Retirement Calculators

Retirement calculators are not merely mathematical tools. They are psychological instruments. People use them to answer deeply emotional questions about freedom security aging and identity. The Dave Ramsey retirement calculator works particularly well because it taps into emotional motivation rather than overwhelming users with technical complexity.

Many Americans fear retirement because they associate it with uncertainty and dependency. Financial calculators transform vague fears into measurable goals. Seeing projected growth over decades creates a sense of possibility. This psychological shift matters because motivation often drives long-term saving behavior more effectively than raw financial knowledge alone.

Behavioral finance research consistently shows that people struggle with delayed gratification. Retirement planning requires sacrificing present consumption for future benefits that may feel emotionally distant. Ramsey’s financial approach simplifies decision-making into clear behavioral habits like debt reduction consistent investing and lifestyle discipline. The calculator reinforces those habits visually.

This is especially relevant in the modern digital economy where consumer spending pressures are constant. Social media encourages comparison-driven spending on luxury lifestyles travel experiences designer products and influencer-inspired purchases. Retirement calculators counterbalance this culture by encouraging long-term asset building instead of short-term consumption.

Interestingly creators and influencers themselves increasingly discuss retirement planning publicly because personal branding alone does not guarantee long-term wealth. Many creators experience income volatility despite high earnings years. Smart influencers now diversify into investments real estate equity ownership and digital businesses specifically to build retirement security beyond social media algorithms.

Dave Ramsey’s Retirement Philosophy Versus Traditional Financial Advisors

One reason the Dave Ramsey retirement calculator sparks debate is because Ramsey’s overall investing philosophy differs from many traditional financial advisors. His approach emphasizes debt elimination aggressive retirement contributions and long-term mutual fund investing. Critics argue that some aspects oversimplify investing realities while supporters praise the accessibility and behavioral effectiveness of his system.

Traditional financial advisors often focus heavily on portfolio diversification tax optimization risk-adjusted returns and personalized retirement withdrawal strategies. Ramsey’s messaging by contrast centers more on financial habits and emotional clarity. He speaks to people who feel financially overwhelmed rather than financially sophisticated.

This distinction matters because most Americans are not investment professionals. They need systems simple enough to maintain consistently over decades. Ramsey’s framework works well for households that need structure and accountability. However high-income entrepreneurs investors or financially advanced users may require more nuanced planning involving estate strategies tax-efficient investing alternative assets or business equity planning.

Modern wealth creation has also evolved beyond traditional retirement account models. Entrepreneurs increasingly build retirement wealth through business ownership startup investments real estate portfolios licensing deals digital products and creator economy monetization. A YouTube creator earning advertising revenue sponsorships and affiliate income may approach retirement planning very differently from a salaried employee with a 401(k).

Still Ramsey’s core principle remains powerful: long-term consistency matters more than chasing financial shortcuts. Many wealthy individuals succeed not because they found perfect investment timing but because they maintained disciplined financial habits over decades.

The Role of Compound Interest in Long-Term Wealth Building

The true power behind the Dave Ramsey retirement calculator is compound interest. This concept remains one of the most important wealth-building mechanisms in modern finance. Compound growth allows invested money to generate earnings that themselves continue generating additional earnings over time.

For younger investors time matters far more than starting balance size. Someone investing modest amounts consistently in their twenties can potentially outperform someone contributing far larger amounts later in life. Retirement calculators visually demonstrate this effect which is why they often create emotional urgency among users who realize the cost of delaying investing.

Compound interest also explains why celebrities entrepreneurs and influencers increasingly diversify income into long-term assets rather than relying solely on active earnings. High-income individuals understand that scalable investments create financial leverage. Real estate appreciation dividend portfolios equity ownership and business investments continue generating wealth long after active work slows down.

The creator economy provides fascinating examples of modern compound wealth strategies. Influencers who once relied entirely on sponsorships now invest in startups launch digital products build subscription communities and purchase real estate assets. These moves transform temporary internet fame into sustainable long-term wealth structures.

Retirement calculators simplify this principle by helping users see how consistent investing grows over decades. While the projections are estimates rather than guarantees they reinforce the financial reality that wealth accumulation usually rewards patience more than speed.

Common Mistakes People Make Using Retirement Calculators

Despite their usefulness retirement calculators can create misleading confidence if users misunderstand their limitations. One of the biggest mistakes people make is assuming projected balances guarantee future financial security. Calculators rely heavily on assumptions regarding investment returns inflation contribution consistency and retirement expenses.

Inflation represents a particularly underestimated threat. A retirement portfolio that appears massive today may provide far less purchasing power decades later. Healthcare costs housing expenses taxes and economic shifts can dramatically alter retirement realities. Many users focus on reaching a certain dollar amount without understanding future living cost dynamics.

Another common mistake involves unrealistic contribution assumptions. People often enter optimistic monthly savings goals during moments of financial motivation but real-life consistency becomes difficult during economic downturns career disruptions or unexpected expenses. Behavioral discipline ultimately matters more than idealized projections.

Entrepreneurs and freelancers face additional challenges because their income streams fluctuate significantly. Traditional calculators assume relatively stable contribution patterns but digital business owners creators and self-employed professionals often experience unpredictable earnings cycles. Retirement planning for these groups requires greater flexibility and emergency reserves.

There is also the issue of overreliance on retirement accounts alone. Modern wealth building increasingly involves diversified asset ownership including real estate business equity private investments royalties and passive income systems. Retirement calculators focusing only on investment accounts may overlook broader wealth-building opportunities.

Retirement Planning in the Creator Economy Era

The creator economy has fundamentally changed how younger generations approach retirement planning. Many digital entrepreneurs no longer expect traditional corporate pensions or long-term employer loyalty. Instead they build income ecosystems combining content monetization affiliate marketing online education consulting e-commerce sponsorships and investment portfolios.

This shift creates both opportunity and risk. Successful creators can potentially generate wealth faster than traditional career paths but income volatility remains extremely high. Algorithms change audiences shift and digital trends evolve rapidly. Retirement planning becomes critical because creator income often lacks the stability and employer benefits associated with traditional jobs.

The Dave Ramsey retirement calculator still provides value for creators because it encourages long-term thinking. However digital entrepreneurs may need more advanced planning strategies involving tax management business structures retirement account optimization and investment diversification. A YouTuber earning fluctuating advertising revenue requires a different financial system than a salaried employee with predictable paychecks.

Celebrity finance trends further illustrate this evolution. Many influencers publicly showcase luxury lifestyles while quietly building backend wealth through equity ownership real estate acquisitions licensing deals and startup investments. Public perception often focuses on visible spending but true financial security usually comes from asset accumulation behind the scenes.

Modern retirement planning increasingly blends entrepreneurship with investing. Wealthy individuals today rarely rely on a single income source. Instead they build layered financial ecosystems designed to generate both active income and passive cash flow over time.

How Inflation and Taxes Impact Retirement Projections

One major criticism of many online retirement calculators is their limited treatment of inflation and taxation. Future retirement balances can appear impressive until users adjust for reduced purchasing power. Inflation quietly erodes wealth over time making realistic retirement planning far more complex than simply targeting a large account balance.

For example a million-dollar retirement target may sound substantial today but decades of inflation can dramatically reduce what that amount actually buys. Housing costs healthcare expenses insurance premiums and basic living costs continue rising over time. Smart retirement planning therefore requires inflation-adjusted thinking rather than focusing purely on nominal balances.

Taxes also play a major role in retirement sustainability. Traditional retirement accounts often involve deferred taxation meaning withdrawals later become taxable income. High-income earners entrepreneurs and investors may need sophisticated tax strategies involving Roth accounts trusts business structures and diversified withdrawal planning.

Financially successful celebrities and entrepreneurs frequently work with wealth managers specifically to protect assets from excessive taxation while maintaining long-term liquidity. Retirement planning at higher wealth levels becomes less about simple saving and more about strategic financial engineering.

Even average households benefit from understanding these principles. The best retirement strategies involve not only accumulating wealth but preserving purchasing power managing taxes efficiently and maintaining adaptable income systems during retirement years.

Should You Trust the Dave Ramsey Retirement Calculator?

The answer depends on how you use it. The Dave Ramsey retirement calculator is highly effective as a motivational and educational tool. It simplifies retirement planning for people who might otherwise avoid investing entirely. It encourages long-term thinking disciplined contributions and financial awareness all of which are valuable.

However users should avoid treating any retirement calculator as a guaranteed financial forecast. Markets fluctuate life circumstances change and economic conditions evolve unpredictably. Retirement planning works best when calculators serve as starting points rather than absolute predictions.

For beginners the calculator offers accessible clarity. For advanced investors entrepreneurs and high-income earners it may function better as a rough projection tool alongside more detailed financial planning systems. Complex wealth-building strategies often require personalized guidance beyond standardized calculators.

Still one of Ramsey’s greatest strengths lies in behavioral finance communication. He understands that financial success depends heavily on mindset and consistency. Many people fail financially not because they lacked technical investment knowledge but because they never developed disciplined financial habits.

In that sense the calculator succeeds because it transforms retirement planning from an intimidating financial problem into an emotionally achievable process.

The Future of Retirement Planning and Digital Wealth Tools

Retirement planning tools are evolving rapidly alongside financial technology innovation. Artificial intelligence automated investing platforms personalized budgeting systems and predictive analytics are transforming how people approach long-term wealth management. Future retirement calculators may incorporate real-time market conditions behavioral spending analysis healthcare forecasting and dynamic income modeling.

At the same time younger generations increasingly value financial independence over traditional retirement itself. Many entrepreneurs and creators aim to build flexible lifestyles supported by passive income rather than waiting for a fixed retirement age. Digital business ownership online assets and scalable investments are reshaping wealth strategies globally.

This trend has fueled explosive growth in financial education content online. Finance influencers investment educators and wealth-building creators now operate massive digital media brands monetized through courses sponsorships affiliate marketing and premium memberships. Retirement planning has become both a financial necessity and a highly profitable content category.

Dave Ramsey’s continued relevance demonstrates how powerful trust-based financial branding can become. Consumers seek guidance from personalities who make complex financial ideas feel emotionally understandable. In an era of economic uncertainty clarity itself has become a valuable product.

The future of retirement planning will likely combine traditional investing principles with more flexible digital wealth-building models. Those who adapt early may build stronger long-term financial resilience than previous generations relying solely on conventional retirement structures.

Conclusion

The Dave Ramsey retirement calculator is far more than a simple online tool. It represents a broader financial philosophy built around discipline consistency and long-term wealth building. Its popularity reflects growing anxiety around retirement security as well as rising demand for accessible financial education in a complicated economic environment.

For beginners the calculator provides clarity and motivation. It helps users visualize compound growth understand the importance of consistent investing and develop stronger financial habits. For more advanced investors and entrepreneurs it can serve as a useful starting point while highlighting the need for broader wealth strategies involving taxes diversification business ownership and passive income systems.

Retirement itself is changing rapidly. The creator economy digital entrepreneurship real estate investing and online business ownership are reshaping how people build long-term financial security. Modern wealth rarely comes from a single paycheck alone. Instead it emerges from diversified assets scalable income streams and disciplined financial management over time.

Ultimately the value of the Dave Ramsey retirement calculator lies not in perfect prediction accuracy but in its ability to encourage action. Financial freedom rarely happens accidentally. It usually begins when people stop avoiding the future and start planning for it intentionally.

FAQs

What is the Dave Ramsey retirement calculator?

The Dave Ramsey retirement calculator is an online financial tool designed to estimate future retirement savings based on factors like age current investments monthly contributions and projected market returns. It helps users visualize long-term wealth growth through compound interest.

Is the Dave Ramsey retirement calculator accurate?

The calculator provides estimates rather than guaranteed results. Its accuracy depends on assumptions regarding investment returns inflation contribution consistency and retirement timelines. It works best as a planning guide rather than an exact financial forecast.

Does the Dave Ramsey retirement calculator account for inflation?

Some versions may include limited inflation considerations but users should still independently evaluate future purchasing power. Inflation can significantly reduce the real value of retirement savings over time.

Can freelancers and creators use the retirement calculator?

Yes but freelancers creators and entrepreneurs should recognize that fluctuating income may require more flexible planning. Variable earnings taxes and business expenses can affect long-term retirement contributions.

What investment return does Dave Ramsey usually assume?

Dave Ramsey often references historically strong stock market returns in his retirement discussions. Critics argue these projections can appear optimistic while supporters believe they encourage consistent long-term investing behavior.

Should I rely only on retirement accounts for wealth building?

Most financial experts recommend diversified wealth-building strategies. Retirement accounts are important but additional assets like real estate business ownership dividend investments and passive income streams can strengthen long-term financial security.

Why are retirement calculators so popular today?

Retirement calculators have become popular because economic uncertainty inflation concerns and declining pension availability have increased demand for accessible financial planning tools. They help users feel more in control of their financial future.

I am a professional finance content writer with expertise in personal finance investing, banking, loans, insurance, credit cards, budgeting, and market related topics. I create clear, SEO optimized, and reader friendly finance content that helps audiences understand complex financial concepts in simple words. My goal is to write trustworthy and engaging content that improves search visibility, builds credibility, and supports business growth.

I am a professional finance content writer with expertise in personal finance investing, banking, loans, insurance, credit cards, budgeting, and market related topics. I create clear, SEO optimized, and reader friendly finance content that helps audiences understand complex financial concepts in simple words. My goal is to write trustworthy and engaging content that improves search visibility, builds credibility, and supports business growth.