Starting a new job in the United States often comes with a stack of paperwork and one document that almost every employee encounters is the W-4 form. Many workers quickly fill it out without fully understanding its purpose but this small form plays a major role in determining how much federal income tax is taken out of each paycheck. If you have ever wondered what is a W4 and why employers require it learning the answer can help you manage your taxes more effectively and avoid financial surprises later.

The W-4 form directly affects your take-home pay your tax refund and even whether you might owe money to the Internal Revenue Service at the end of the year. Understanding how the form works is important for full-time employees part-time workers freelancers transitioning into traditional employment and anyone beginning a new position. A properly completed W-4 can help you maintain better financial stability throughout the year instead of dealing with unexpected tax bills.

Many Americans misunderstand the purpose of the form because tax terminology can feel complicated. However the process becomes much easier once you understand the basics. The form is not designed to punish employees or confuse taxpayers. Instead it acts as a guide that tells employers how much federal income tax should be withheld from wages before employees receive their paychecks.

In this detailed guide you will learn everything you need to know about the W-4 form including its purpose how to fill it out correctly common mistakes people make and how it influences your yearly taxes. By the end of this article you will have a clear understanding of how to use the form wisely and confidently.

Understanding the Purpose of a W-4 Form

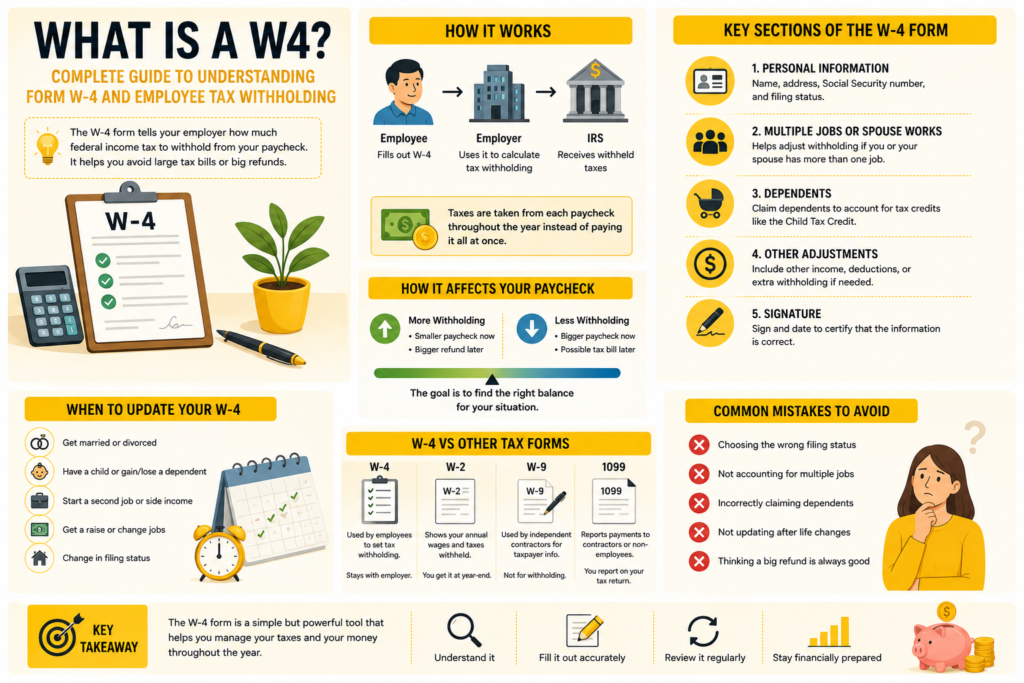

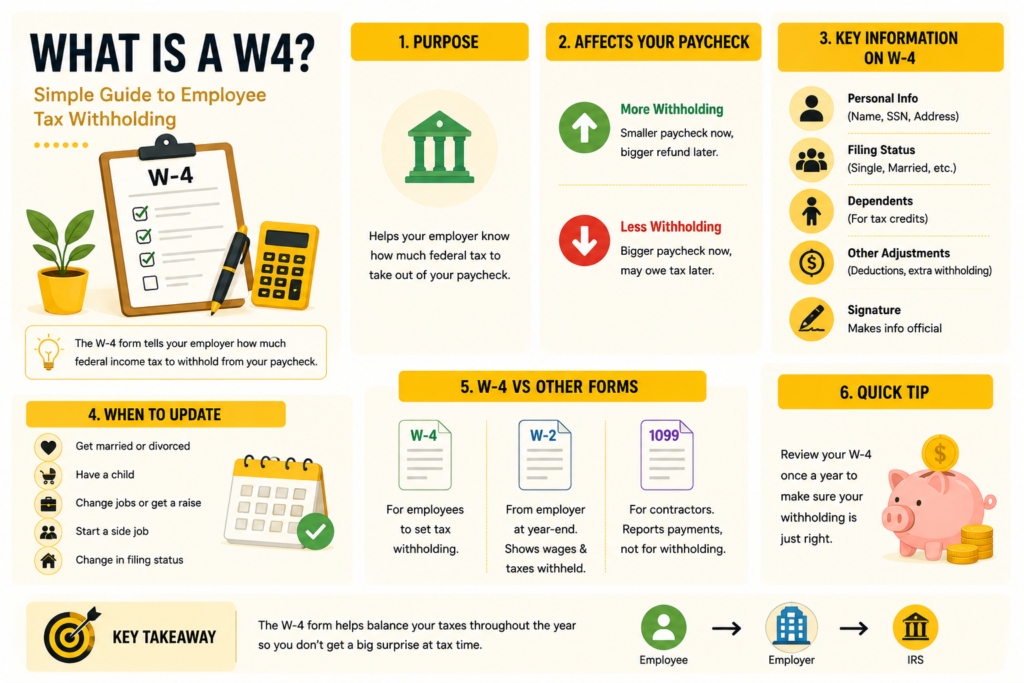

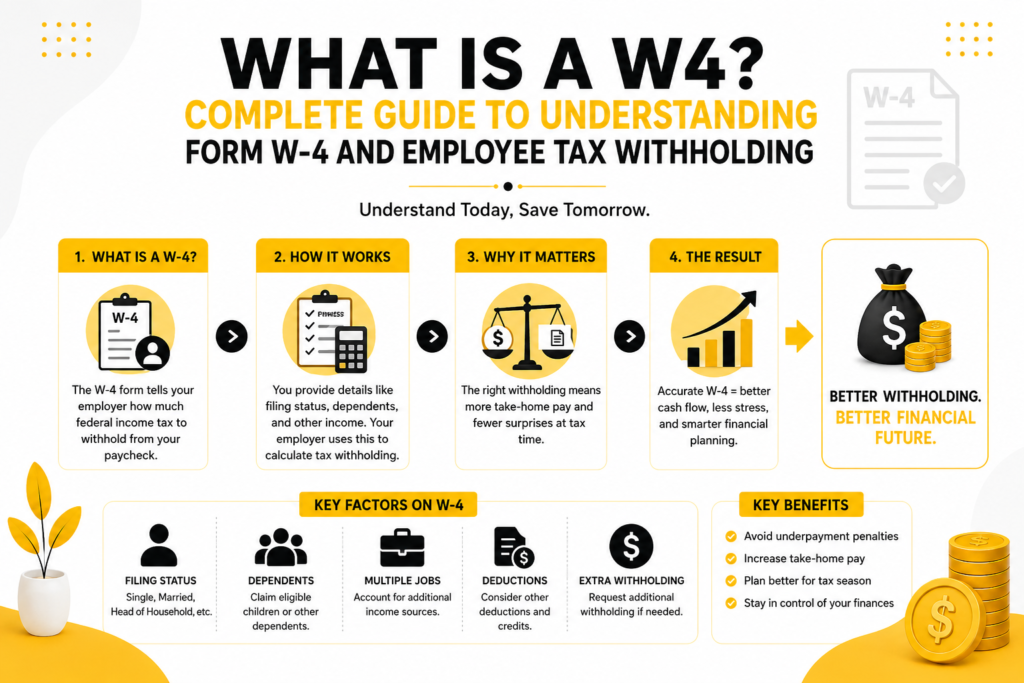

The W-4 form officially known as the Employee’s Withholding Certificate is a tax document used in the United States by employers to determine how much federal income tax should be withheld from an employee’s paycheck. Every time an employee receives wages the employer sends a portion of those earnings to the IRS on the employee’s behalf. The W-4 form helps calculate the correct amount.

The main reason the government uses withholding is to collect taxes gradually throughout the year rather than requiring taxpayers to pay everything in one large amount during tax season. This system helps employees manage tax obligations in smaller portions while ensuring the government receives a steady flow of revenue. Without withholding many people might struggle to pay large tax bills annually.

When someone asks what is a W4 the simplest explanation is that it is an instruction form employees give to employers for tax withholding purposes. It allows workers to indicate financial details that influence their expected tax liability. These details may include filing status dependents multiple jobs deductions or additional income sources.

The information entered on the form affects the balance between the amount withheld and the amount ultimately owed when filing an annual tax return. If too little tax is withheld the employee may owe money later. If too much is withheld the employee may receive a tax refund. Understanding this balance is one of the most important aspects of managing personal finances in the United States.

The History and Evolution of the W-4 Form

The W-4 form has existed for decades but it has evolved significantly over time. Earlier versions of the form relied heavily on withholding allowances. Employees claimed allowances based on dependents and financial situations and those allowances determined withholding amounts. While the older system worked for many years it eventually became outdated and confusing for taxpayers.

The passage of major tax reforms in the United States created a need for modernization. In response the IRS redesigned the form beginning in 2020. The updated version removed withholding allowances entirely and replaced them with a more straightforward method focused on actual income dependents and deductions. This change aimed to improve accuracy and reduce taxpayer confusion.

The redesigned form also attempted to reflect modern employment realities. Many households today include multiple earners side income freelance work or changing financial situations throughout the year. The new structure makes it easier for employees to account for these variables when determining withholding preferences.

Although the updated form initially caused uncertainty among workers familiar with the old system most taxpayers now find it easier to understand after reviewing the instructions carefully. Employers and payroll departments also adapted their systems to accommodate the revised format. Today’s W-4 is designed to provide more precise withholding estimates and minimize large tax surprises.

How the W-4 Form Impacts Your Paycheck

One of the most important things to understand about the W-4 form is how directly it influences your paycheck. Every time you receive wages your employer calculates federal tax withholding using the information provided on your form. That means even small adjustments on the document can noticeably change your take-home pay.

If you choose to have more taxes withheld your paycheck becomes smaller throughout the year but you may receive a larger refund during tax season. Some workers prefer this approach because it creates a form of forced savings. Receiving a refund can feel financially rewarding and may help with large expenses or savings goals.

On the other hand if you reduce withholding your paycheck becomes larger because less money is sent to the IRS. While this increases immediate cash flow it also raises the possibility of owing taxes later. For individuals with tight monthly budgets the increased paycheck amount may be helpful but careful planning becomes essential to avoid unexpected bills.

The relationship between withholding and refunds often confuses taxpayers. A large refund does not necessarily mean someone paid fewer taxes overall. Instead it usually means they overpaid throughout the year and are receiving the difference back from the government. Understanding this concept helps workers make smarter financial decisions when completing their W-4 forms.

Key Sections Included on the W-4 Form

The modern W-4 form contains several important sections that employees should understand before filling it out. Each section plays a specific role in determining withholding accuracy. Taking the time to complete the form carefully can improve financial planning and reduce tax complications later.

The first section requests basic personal information such as name address Social Security number and filing status. Filing status options typically include single married filing jointly head of household or other tax categories recognized by the IRS. Choosing the correct status is essential because it affects withholding calculations.

Another major section addresses multiple jobs or working spouses. Households with more than one source of income often require adjusted withholding to avoid underpayment. The form includes worksheets and calculation tools designed to help employees estimate appropriate withholding amounts in these situations.

The dependents section allows employees to claim qualifying children or other eligible dependents for tax credit purposes. Tax credits can significantly reduce tax liability which means withholding adjustments may also be appropriate. Employees can also list additional deductions or extra withholding requests if they expect complex tax situations during the year.

Finally employees sign the form to confirm that the information provided is accurate. Employers then use the completed document to configure payroll withholding settings. Reviewing these sections carefully ensures the form reflects current financial circumstances accurately.

Common Mistakes People Make When Filling Out a W-4

Many employees complete the W-4 form too quickly without understanding the consequences of inaccurate information. One of the most common mistakes is selecting the wrong filing status. Some workers choose a status based on assumptions rather than actual IRS rules which can create withholding errors throughout the year.

Another frequent issue involves failing to account for multiple jobs. In households where both spouses work or where individuals hold side jobs withholding calculations become more complicated. Ignoring additional income sources can result in insufficient withholding and unexpected tax bills during filing season.

Some employees also misunderstand the purpose of claiming dependents. Listing dependents affects withholding because certain tax credits reduce overall tax liability. However claiming dependents incorrectly or exaggerating eligibility may lead to underpayment problems and possible IRS penalties later.

People often forget to update their W-4 forms after major life events. Marriage divorce childbirth job changes or significant income increases can all affect withholding needs. Continuing to use outdated information may create financial imbalances that become apparent only when filing taxes.

Another mistake involves assuming a large refund is always beneficial. While refunds can feel satisfying they may indicate that too much money was withheld throughout the year. Employees sometimes unintentionally reduce their available monthly income by over-withholding taxes unnecessarily.

When You Should Update Your W-4 Form

Many employees complete a W-4 only when starting a new job but updating the form periodically is often necessary. Financial circumstances can change significantly over time and withholding should ideally reflect those changes as accurately as possible.

Marriage is one of the most common reasons to revise a W-4 form. Married couples may qualify for different tax brackets deductions or credits compared to single filers. Updating withholding after marriage helps ensure taxes are calculated correctly based on household income.

Having children also affects tax liability because parents may qualify for valuable tax credits and deductions. Employees who become parents often adjust their W-4 forms to reduce withholding appropriately. This change may increase take-home pay while reflecting lower anticipated tax obligations.

Job transitions are another important reason to revisit withholding. Starting a second job switching employers or receiving a substantial raise can alter tax calculations. Employees with multiple income streams should especially review withholding to avoid underpayment issues.

Divorce separation or changes in dependent status can also require updates. Tax laws and financial situations evolve over time making periodic reviews beneficial. Many financial experts recommend checking W-4 information annually or after any major life event to maintain accurate withholding.

The Difference Between a W-4 and Other Tax Forms

Tax documents can seem overwhelming because many forms have similar names and purposes. Understanding the difference between a W-4 and other common tax forms helps reduce confusion and improves financial literacy.

The W-4 form is used for withholding instructions during employment. Employees complete it at the beginning of a job or when adjusting withholding preferences. It stays with the employer and generally is not submitted directly with annual tax returns.

A W-2 form is different because employers provide it to employees at the end of the year. The W-2 summarizes annual wages taxes withheld and other payroll information. Employees use this form when preparing federal and state tax returns.

Independent contractors and freelancers often encounter the W-9 form instead of a W-4. A W-9 collects taxpayer identification information for reporting purposes but does not involve withholding instructions. Contractors are usually responsible for paying their own estimated taxes rather than relying on employer withholding.

The 1099 form is another important distinction. Businesses issue 1099 forms to independent contractors and certain non-employees to report payments made during the year. Unlike traditional employees recipients of 1099 income generally manage their own tax obligations without payroll withholding.

Understanding these differences helps workers choose the correct forms based on employment type and tax responsibilities. It also prevents misunderstandings that could create filing issues or withholding problems.

How to Fill Out a W-4 Form Correctly

Completing a W-4 accurately requires attention to detail and a basic understanding of personal financial circumstances. Although the form may initially appear intimidating following a step-by-step approach makes the process much more manageable.

Begin by entering personal information exactly as it appears on official documents. Accurate names addresses and Social Security numbers help prevent payroll processing issues and IRS mismatches. Employees should also carefully choose the correct filing status based on current tax rules.

If you have multiple jobs or a working spouse the next step becomes especially important. The form includes guidance designed to estimate combined withholding needs across different income sources. Using the IRS withholding estimator can improve accuracy significantly in these situations.

The dependents section requires calculating eligible tax credits. Employees with children or qualifying dependents should follow IRS instructions carefully to avoid overstating credits. Accurate calculations help create balanced withholding throughout the year.

Additional deductions and extra withholding can also be included. Some taxpayers prefer extra withholding if they expect investment income freelance earnings or other taxable income not subject to payroll withholding. Others may reduce withholding if they qualify for substantial deductions.

After completing the form employees should review every section carefully before signing. Even small errors can influence withholding outcomes. Keeping a personal copy of the completed form is also helpful for future reference and financial planning.

Understanding Tax Refunds and Tax Bills Through the W-4

Many people associate tax season with either receiving a refund or owing money to the IRS. The W-4 form plays a major role in determining which outcome occurs. Understanding this relationship helps employees make informed withholding decisions.

A tax refund occurs when more taxes were withheld throughout the year than the taxpayer ultimately owed. The IRS returns the excess amount after the annual return is processed. While refunds are common they simply represent overpaid taxes rather than bonus income.

Some employees intentionally over-withhold because they prefer receiving a lump sum refund. This strategy can help individuals save money indirectly especially if they struggle with budgeting discipline. However others prefer maximizing monthly cash flow instead of waiting for refunds.

Tax bills happen when withholding was insufficient to cover total tax liability. This may occur because of inaccurate W-4 information multiple jobs investment income freelance work or changing financial circumstances during the year. Owing taxes is not necessarily negative but unexpected bills can create financial stress.

Balancing withholding accurately is usually the ideal approach. Proper withholding allows employees to maintain steady monthly income while minimizing surprises during tax season. The IRS withholding estimator and periodic paycheck reviews can help workers adjust their W-4 forms effectively.

Why Freelancers and Gig Workers View W-4 Forms Differently

Freelancers independent contractors and gig workers operate under different tax systems compared to traditional employees. Since they usually do not receive regular payroll withholding they may not use W-4 forms directly. However understanding the concept behind withholding remains extremely important.

Traditional employees rely on employers to calculate and submit taxes automatically. In contrast freelancers often make quarterly estimated tax payments to the IRS. Because no employer manages withholding independent workers must budget carefully for taxes throughout the year.

Some gig workers transition between freelance and traditional employment. In these cases understanding what is a W4 becomes especially valuable because withholding may need adjustments to account for self-employment income. Employees with side businesses often underestimate taxes if they rely only on standard payroll withholding.

Freelancers also experience different financial challenges related to inconsistent income. While traditional employees usually receive predictable paychecks contractors may earn fluctuating amounts monthly. This variability makes tax planning more complicated and increases the importance of careful recordkeeping.

Workers moving from independent contracting into salaried employment often appreciate the simplicity of automatic withholding once they understand how the W-4 system works. Although taxes remain unavoidable withholding helps distribute obligations more evenly across the year.

Digital Payroll Systems and Modern W-4 Management

Technology has transformed payroll management significantly over the past decade. Many employers now use digital onboarding systems that allow employees to complete W-4 forms electronically rather than on paper. These systems streamline tax withholding processes while improving record accuracy.

Online payroll platforms often guide employees through each section with explanations and automated calculations. Some systems even integrate IRS withholding tools to help workers estimate appropriate withholding levels more accurately. This reduces confusion and decreases the likelihood of major errors.

Employees can also update withholding preferences more conveniently through online HR portals. Instead of waiting for paper forms workers can often submit electronic changes after major life events such as marriage childbirth or salary increases. Faster updates improve withholding responsiveness throughout the year.

Digital payroll systems additionally improve transparency. Employees can review paycheck deductions withholding totals and tax records more easily than ever before. This accessibility encourages greater financial awareness and helps workers understand how withholding decisions affect income.

Despite these technological improvements many employees still misunderstand withholding basics. Digital convenience cannot replace financial education entirely. Workers who understand the reasoning behind W-4 adjustments are better equipped to make smart payroll decisions regardless of whether forms are submitted electronically or manually.

Financial Planning Strategies Related to W-4 Withholding

The W-4 form can serve as a useful financial planning tool when used strategically. Instead of viewing withholding as a routine payroll requirement many financially savvy individuals treat it as part of broader money management planning.

Employees who anticipate significant deductions or credits may reduce withholding to increase monthly cash flow. This strategy can provide extra funds for investments debt repayment or emergency savings throughout the year. However careful calculations are essential to avoid underpayment penalties.

Others prefer conservative withholding to reduce tax-season anxiety. Receiving a moderate refund can create a sense of financial security especially for households with variable expenses. While this approach means temporarily giving the government interest-free money some taxpayers value the predictability it provides.

People with side businesses or investment income often increase withholding intentionally. Since additional income sources may not have automatic tax withholding adjusting payroll deductions helps offset future liabilities. This strategy can simplify quarterly tax planning and reduce surprise bills.

Financial advisors frequently encourage annual withholding reviews. Tax laws change regularly and personal financial circumstances evolve over time. Reviewing W-4 settings during yearly budgeting discussions helps maintain accurate withholding while supporting broader financial goals.

How the IRS Uses W-4 Information

The IRS does not use W-4 forms to judge spending habits or monitor personal lifestyles. Instead the information primarily supports accurate tax collection throughout the year. Employers use the data to calculate withholding according to IRS tax tables and payroll regulations.

The IRS designed the form to balance efficiency and fairness within the tax system. Without withholding guidance employers would struggle to estimate appropriate payroll deductions consistently. The W-4 helps standardize withholding calculations across millions of workers nationwide.

Although the form contains financial information employees are not required to disclose every aspect of their personal lives. The document focuses specifically on factors that affect withholding calculations such as filing status dependents deductions and multiple jobs.

The IRS may compare withholding records with annual tax returns to identify discrepancies. Significant inconsistencies could trigger additional review or notices requesting clarification. However ordinary withholding adjustments generally do not create problems when completed honestly and accurately.

Employees should remember that the goal of the W-4 system is not to maximize refunds or create hardship. Instead it aims to align withholding closely with actual tax liability. Understanding this purpose helps workers approach the form more confidently and strategically.

Conclusion

Understanding what is a W4 is an essential part of managing personal finances and navigating employment in the United States. Although the form may appear simple at first glance it has a direct impact on paycheck amounts annual tax obligations and overall financial planning.

The W-4 form exists to help employers calculate appropriate federal income tax withholding throughout the year. By providing accurate information about filing status dependents deductions and multiple jobs employees can reduce the likelihood of owing unexpected taxes or overpaying significantly.

Modern versions of the form are designed to improve clarity and reflect today’s more complex financial realities. Whether someone works a single job manages multiple income streams or transitions between freelance and salaried work understanding withholding remains extremely important.

Regularly reviewing and updating W-4 information after major life events can help maintain accurate withholding and improve financial stability. Marriage children raises job changes and side income can all affect tax liability and should prompt reconsideration of withholding settings.

Ultimately the W-4 form is more than just employment paperwork. It is a practical financial tool that influences budgeting tax refunds and long-term money management. Employees who understand how the form works are better equipped to make informed decisions and avoid unnecessary financial stress during tax season.

FAQs

What is a W4 form used for?

A W-4 form is used by employers to determine how much federal income tax should be withheld from an employee’s paycheck. The information employees provide helps employers calculate payroll deductions accurately.

Do I need to fill out a W-4 every year?

Most employees do not need to complete a new W-4 every year unless their financial situation changes. However reviewing withholding annually is a smart practice to ensure accuracy.

Can changing my W-4 increase my paycheck?

Yes adjusting your W-4 can increase your paycheck if you reduce withholding. However lower withholding may also increase the risk of owing taxes later during tax season.

What happens if I fill out my W-4 incorrectly?

Incorrect information may lead to too much or too little tax withholding. This can result in smaller paychecks reduced refunds or unexpected tax bills when filing annual returns.

Is a W-4 the same as a W-2?

No they are different forms. A W-4 is completed by employees to guide withholding while a W-2 is issued by employers at the end of the year to summarize wages and taxes withheld.

Should freelancers use a W-4 form?

Freelancers and independent contractors usually do not use W-4 forms because taxes are not withheld automatically. Instead they often make estimated quarterly tax payments directly to the IRS.

How often can I change my W-4?

Employees can update their W-4 whenever necessary. Many people revise the form after major life events such as marriage divorce childbirth or significant income changes.