What Is Deferred Revenue?

Deferred revenue is money a company receives from customers before delivering goods or services. Because the company has not yet fulfilled its obligations the payment cannot immediately be recognized as earned revenue. Instead it is recorded as a liability on the balance sheet until the company provides the promised products or services.

In accounting deferred revenue is often called unearned revenue. It represents a future obligation to customers. Once the company delivers the service or product the liability decreases and revenue is recognized in the income statement.

Deferred revenue plays a critical role in accrual accounting because it ensures businesses recognize income only when it is earned rather than when cash is received. This practice improves financial reporting accuracy and helps stakeholders evaluate a company’s true performance.

Examples of deferred revenue include software subscriptions annual maintenance contracts prepaid insurance premiums gym memberships airline tickets and magazine subscriptions.

How Deferred Revenue Works in Accounting

Deferred revenue follows the revenue recognition principle under accrual accounting. According to this principle revenue should be recognized only when earned regardless of when payment is received.

Imagine a customer pays $1200 for a one-year software subscription. The company initially records the entire amount as deferred revenue because the service has not yet been delivered. Each month as services are provided $100 is recognized as earned revenue.

This process ensures financial statements accurately reflect economic activity over time. Investors and analysts rely on this approach to assess recurring revenue streams and operational performance.

Businesses that receive advance payments frequently manage large deferred revenue balances. Subscription-based companies SaaS providers and membership organizations are especially affected.

Why Deferred Revenue Matters for Businesses

Deferred revenue provides valuable insights into a company’s future earnings potential. A growing deferred revenue balance may indicate strong sales and customer demand particularly in subscription businesses.

For investors deferred revenue can be a sign of future cash flow stability. Companies with predictable recurring payments often enjoy more stable financial performance and higher valuations.

From a compliance perspective proper handling of deferred revenue is essential for meeting accounting standards such as GAAP and IFRS. Misreporting revenue can lead to inaccurate financial statements and regulatory penalties.

Deferred revenue also improves cash management because businesses receive payment before incurring all service delivery costs. This additional liquidity can support operations and expansion.

Deferred Revenue on the Balance Sheet

Deferred revenue appears as a liability because the company owes goods or services to customers. It is usually classified as either current or long-term liability depending on when the obligation will be fulfilled.

If the service is expected to be delivered within one year deferred revenue is listed as a current liability. If fulfillment extends beyond one year part of the balance may be classified as a long-term liability.

As services are delivered the liability decreases while revenue increases. This movement directly affects both the balance sheet and income statement.

Understanding where deferred revenue appears on financial statements helps investors evaluate future earnings and business health.

Deferred Revenue Recognition Process

Revenue recognition begins when a customer prepays for goods or services. At this stage cash increases but earned revenue does not.

Over time as obligations are fulfilled portions of deferred revenue move from liabilities to revenue. This systematic approach aligns income with service delivery periods.

Accounting frameworks such as IFRS 15 and ASC 606 provide guidelines for determining when revenue can be recognized. These standards emphasize identifying performance obligations and recognizing revenue as those obligations are satisfied.

Proper recognition prevents companies from overstating profits and ensures consistent financial reporting.

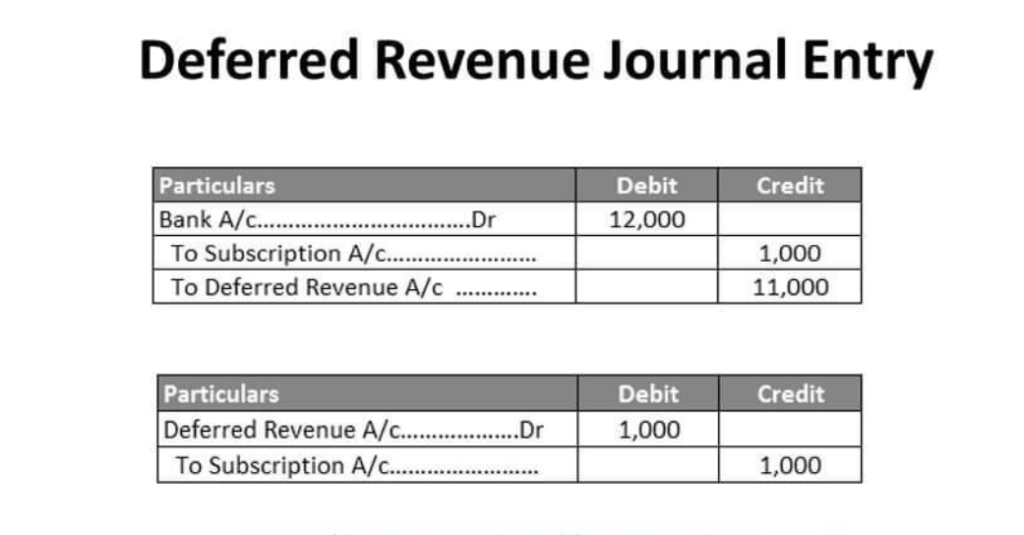

Journal Entries for Deferred Revenue

Recording deferred revenue requires specific journal entries. Initially when payment is received:

Journal Entry:

Debit: Cash …………… $1200

Credit: Deferred Revenue … $1200

This entry increases cash while creating a liability.

After one month of service delivery:

Debit: Deferred Revenue … $100

Credit: Revenue ………… $100

This process repeats until the entire amount has been recognized as earned revenue.

Accurate journal entries are essential for maintaining reliable financial records and complying with accounting standards.

Real-World Examples of Deferred Revenue

Deferred revenue exists across many industries. Subscription businesses are among the most common examples.

A streaming platform that charges customers annually records the payment as deferred revenue and recognizes it monthly over the subscription period.

Airlines record ticket sales as deferred revenue until passengers complete their flights. Similarly gyms recognize membership fees gradually as members use services.

Insurance companies also rely heavily on deferred revenue because policyholders often pay premiums in advance for future coverage periods.

These examples demonstrate how deferred revenue supports accurate financial reporting in various sectors.

Deferred Revenue vs Accrued Revenue

Deferred revenue and accrued revenue are often confused but they represent opposite accounting situations.

Deferred revenue occurs when a company receives payment before delivering goods or services. Accrued revenue occurs when a company has delivered goods or services but has not yet received payment.

Deferred revenue is recorded as a liability because obligations remain outstanding. Accrued revenue is recorded as an asset because payment is expected in the future.

Understanding this distinction is essential for accounting students business owners and financial analysts.

Deferred Revenue vs Accounts Receivable

Accounts receivable and deferred revenue also differ significantly.

Accounts receivable arise when customers owe money for products or services already delivered. Deferred revenue arises when customers pay before receiving products or services.

Accounts receivable are assets because they represent expected cash inflows. Deferred revenue is a liability because it represents future obligations.

Businesses must properly classify these accounts to ensure accurate financial reporting.

Industries That Commonly Use Deferred Revenue

Several industries rely extensively on deferred revenue accounting.

Software-as-a-Service companies receive subscription fees in advance and recognize revenue over contract periods. Media companies use deferred revenue for subscriptions and memberships.

Educational institutions collect tuition before classes begin. Airlines sell tickets before flights occur. Insurance companies receive premiums before coverage periods.

The rise of subscription-based business models has made deferred revenue increasingly important across the global economy.

Benefits and Challenges of Deferred Revenue

Deferred revenue offers many benefits to businesses. Advance payments improve cash flow and provide financial stability. Predictable recurring revenue supports budgeting and strategic planning.

However managing deferred revenue can be challenging. Companies must track performance obligations carefully and comply with complex accounting standards.

Errors in revenue recognition may result in misstated earnings and regulatory concerns. Businesses often use specialized accounting software to automate deferred revenue management.

Balancing compliance with operational efficiency remains a key priority for finance teams.

Latest Update on Deferred Revenue Standards

Modern accounting standards such as ASC 606 in the United States and IFRS 15 internationally have significantly changed revenue recognition practices.

These standards emphasize identifying performance obligations and recognizing revenue when control transfers to customers. Businesses must carefully evaluate contracts to determine appropriate recognition timing.

Regulators continue to focus on transparent reporting especially for subscription-based companies and SaaS businesses.

Organizations should regularly review accounting policies to ensure compliance with evolving standards and best practices.

Common Mistakes Businesses Make

Many businesses incorrectly recognize revenue immediately after receiving cash. This practice violates accrual accounting principles and can overstate earnings.

Another common mistake involves failing to allocate revenue across multiple performance obligations in complex contracts.

Companies may also struggle with long-term contracts that require judgment regarding timing and recognition.

Regular audits strong internal controls and modern accounting systems help reduce these errors.

Best Practices for Managing Deferred Revenue

Businesses should implement robust accounting systems capable of automating revenue recognition schedules.

Clear documentation of customer contracts is essential for identifying performance obligations and recognition periods.

Finance teams should receive regular training on accounting standards to maintain compliance and accuracy.

Periodic reconciliations ensure deferred revenue balances align with actual obligations improving financial transparency.

Conclusion

Deferred revenue is one of the most important concepts in modern accounting and financial reporting. It represents customer payments received before products or services are delivered and is recorded as a liability until obligations are fulfilled.

Understanding deferred revenue helps businesses maintain compliance with accounting standards improve financial transparency and manage recurring revenue effectively. Investors also monitor deferred revenue because it can indicate future earnings potential and business growth.

As subscription-based business models continue to expand deferred revenue will remain a critical metric for companies across industries. By applying proper accounting practices businesses can ensure accurate reporting build trust with stakeholders and support long-term success.

FAQS

Is deferred revenue an asset or liability?

Deferred revenue is a liability because the company still owes goods or services to customers.

Is deferred revenue the same as unearned revenue?

Yes. Deferred revenue and unearned revenue are generally used interchangeably in accounting.

Why is deferred revenue important?

It ensures companies recognize revenue only when earned improving financial accuracy.

Can deferred revenue become earned revenue?

Yes. As products or services are delivered deferred revenue is recognized as earned revenue.

Which industries use deferred revenue most?

Software insurance airlines media subscriptions and education frequently use deferred revenue accounting.

How does deferred revenue affect cash flow?

It increases cash flow immediately because customers pay before receiving services.

Does deferred revenue appear on the income statement?

Initially no. It appears as a liability until recognized as earned revenue.

What accounting standards govern deferred revenue?

ASC 606 and IFRS 15 provide guidance for revenue recognition and deferred revenue accounting.

I am a professional web developer with strong expertise in digital marketing, SEO, and content writing. I specialize in building modern, responsive, and user-friendly websites that deliver performance and results. Along with development skills, I have a deep understanding of search engine optimization strategies and online marketing techniques that help businesses grow their online presence. My goal is to create impactful digital solutions that combine creativity, functionality, and visibility for better user engagement and business success.