Money management begins with understanding how income works yet many people confuse gross income with net income. These two financial terms appear on paychecks tax documents loan applications and business reports but they represent very different amounts of money. Knowing the difference between them can help individuals create realistic budgets prepare taxes accurately and make smarter financial decisions.

The topic of net income vs gross income is especially important in today’s economy where people carefully track expenses savings and investments. Employees often focus on their salary offer without realizing how deductions affect take-home pay. Business owners may celebrate high revenue figures without understanding actual profit margins. Whether you are an employee freelancer entrepreneur or student learning personal finance understanding these terms can improve your financial awareness and planning.

Gross income generally refers to the total amount earned before deductions while net income represents the amount left after taxes and expenses are removed. Although the difference sounds simple its impact reaches nearly every part of financial life. Mortgage approvals tax calculations budgeting and investment decisions all depend on understanding these figures properly.

This guide explores every aspect of net income vs gross income in detail. You will learn how they are calculated where they appear why they matter and how they influence both personal and business finances. By the end of this article you will have a complete understanding of these essential financial concepts.

What Gross Income Means

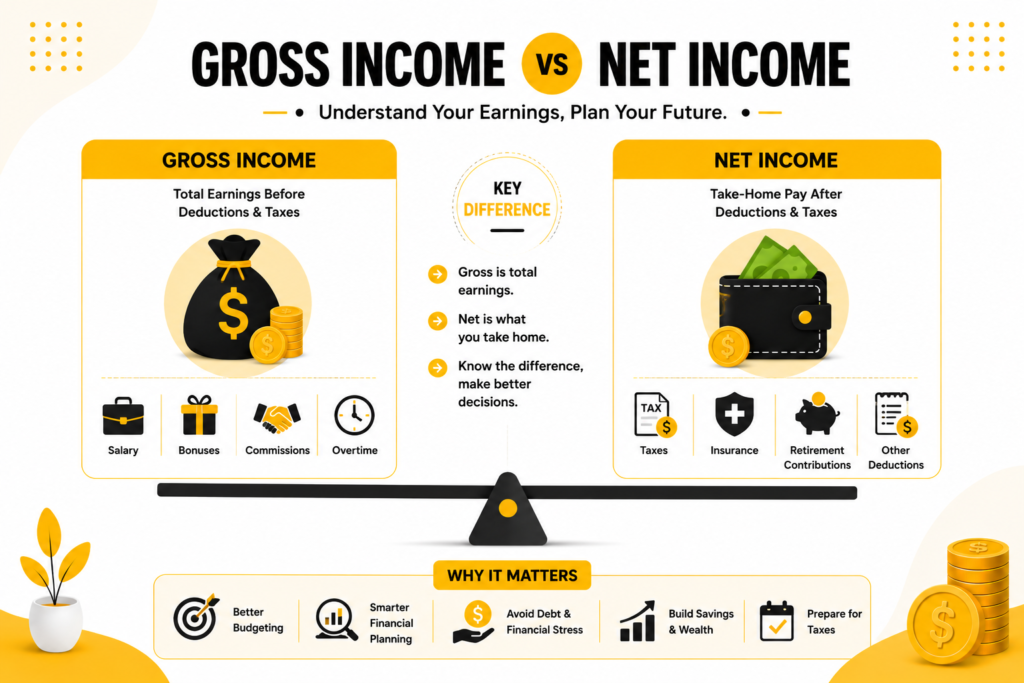

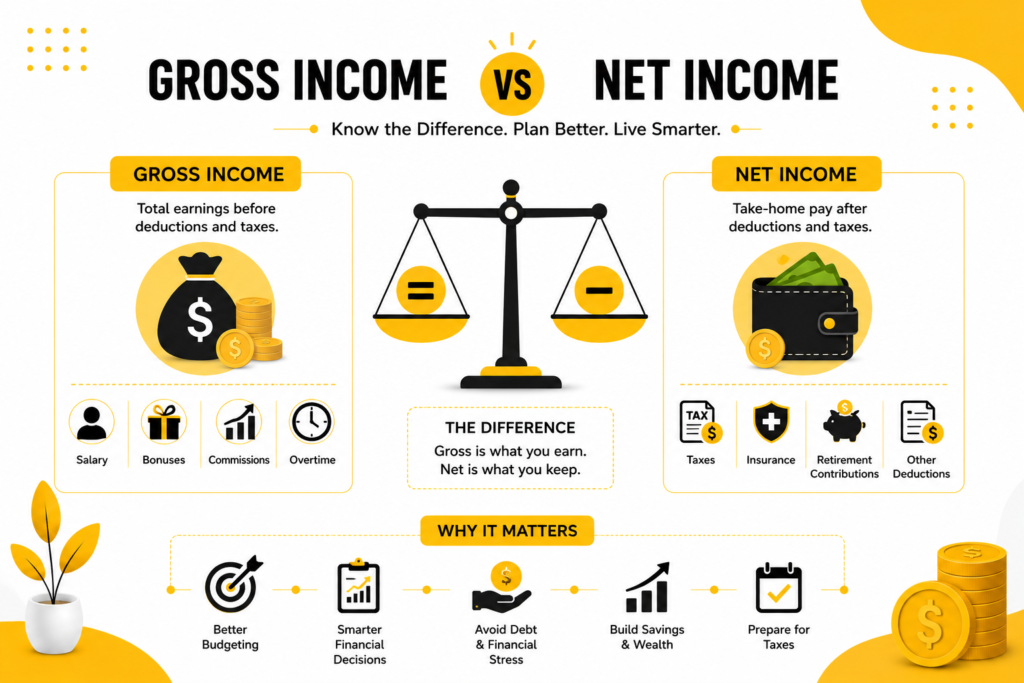

Gross income is the total amount of money earned before any deductions taxes or expenses are subtracted. For employees this includes wages salaries overtime commissions bonuses and other earnings before payroll taxes and benefits are withheld. Businesses also use gross income to describe revenue remaining after subtracting the direct cost of producing goods or services.

Many people first encounter gross income when accepting a job offer. Employers typically advertise annual salaries using gross figures because they represent the full compensation package before deductions. For example if someone earns $60000 annually that amount reflects gross income rather than actual take-home pay. The employee will eventually receive less after federal taxes state taxes health insurance and retirement contributions are deducted.

Gross income is also important for lenders and financial institutions. Banks often evaluate a borrower’s gross monthly income when deciding eligibility for loans or mortgages. This figure helps lenders estimate repayment ability because it shows the total earning potential before expenses reduce disposable income. Credit card companies landlords and car dealerships may also request gross income information during applications.

For businesses gross income represents a slightly different concept. It is often calculated as total revenue minus the cost of goods sold. This helps companies measure profitability before accounting for operating expenses taxes and administrative costs. Understanding gross income allows business owners to analyze sales performance and pricing strategies more effectively.

What Net Income Means

Net income is the amount of money left after all deductions expenses and taxes have been removed from gross income. It is commonly referred to as take-home pay for individuals and profit for businesses. Net income provides a more realistic picture of actual financial resources because it reflects what remains available to spend save or invest.

Employees usually focus on net income once they begin receiving paychecks. Even if a salary appears attractive during hiring negotiations deductions can significantly reduce the final amount deposited into a bank account. Payroll taxes health insurance premiums retirement plan contributions and other withholdings all decrease gross earnings to arrive at net income.

For example an employee earning $5000 monthly in gross pay may only receive $3900 after deductions. This lower figure represents net income and determines how much money can realistically be used for rent groceries transportation entertainment and savings goals. Budgeting based on gross income instead of net income often leads to financial stress because actual available funds are lower.

In the business world net income measures profitability after all expenses have been subtracted from revenue. Operating costs salaries taxes rent utilities marketing and loan interest all affect final profit levels. Investors and analysts frequently examine net income because it reveals how efficiently a company manages expenses while generating earnings.

Net income is one of the most important indicators of financial health. Individuals use it to build budgets and savings plans while companies use it to assess profitability and future growth opportunities. Without understanding net income it becomes difficult to evaluate true financial performance.

Key Differences Between Net Income and Gross Income

The main distinction between net income and gross income lies in deductions and expenses. Gross income reflects total earnings before reductions while net income shows what remains afterward. Although the difference may appear straightforward the financial implications are significant in both personal and business finance.

Gross income is always higher because it represents the starting amount before taxes and deductions. Net income is lower because it accounts for payroll taxes insurance costs retirement contributions and other obligations. For businesses gross income focuses on revenue after production costs while net income measures overall profitability after all expenses are paid.

Another important difference involves financial planning. Gross income helps measure earning potential and overall revenue generation. Net income however is more practical for budgeting because it reflects actual available funds. Someone may earn a high gross salary but struggle financially if deductions and expenses consume most of their income.

Tax treatment also separates these concepts. Governments often calculate tax obligations using gross income as a starting point. Various deductions and credits are then applied to determine taxable income and eventually net earnings. This process explains why understanding both figures is essential during tax season.

The debate around net income vs gross income becomes especially relevant when comparing salaries or evaluating job offers. A position with higher gross pay may not always result in better financial outcomes if deductions are larger. Employees should evaluate benefits tax implications and healthcare costs to understand actual net earnings before making career decisions.

Businesses face similar considerations. A company may report impressive gross revenue but still operate at a loss if expenses remain too high. Investors often prioritize net income because it provides a clearer measure of sustainable profitability.

How Gross Income Is Calculated

Calculating gross income is usually straightforward because it involves adding together all earnings before deductions occur. Employees can determine gross income by multiplying hourly wages by hours worked or by using annual salary figures provided by employers. Additional earnings such as overtime commissions and bonuses are also included.

For hourly workers the calculation begins with regular wages. Someone earning $25 per hour and working 40 hours weekly would generate $1000 in gross weekly income before taxes. If overtime pay or bonuses are added the total gross amount increases accordingly. Salaried employees can divide annual earnings by pay periods to estimate gross monthly or biweekly income.

Self-employed individuals and freelancers calculate gross income differently. They add together all payments received from clients before subtracting business expenses or taxes. This figure represents total business revenue generated during a specific period.

Businesses calculate gross income using a formula based on revenue and production costs. The common formula is:

\text{Gross Income} = \text{Revenue} – \text{Cost of Goods Sold}

This formula helps companies understand how much money remains after covering direct production expenses. Retail stores manufacturers and service providers all rely on this calculation to evaluate operational performance.

Gross income calculations are important because they establish the foundation for taxes financial analysis and budgeting. Accurate calculations ensure individuals and businesses can better plan expenses estimate liabilities and track financial growth over time.

How Net Income Is Calculated

Net income calculations involve subtracting deductions taxes and expenses from gross income. For individuals this includes payroll taxes retirement contributions insurance premiums and other withholdings. Businesses subtract operating expenses taxes and additional costs to determine profitability.

The basic formula for personal net income is:

\text{Net Income} = \text{Gross Income} – \text{Taxes} – \text{Deductions}

For example if an employee earns $4500 monthly in gross pay and pays $1000 in taxes and deductions the remaining $3500 becomes net income. This amount reflects actual take-home pay available for daily living expenses and savings.

Businesses use a broader calculation because they must account for numerous operating costs. Rent employee wages marketing expenses utilities loan interest and taxes all reduce gross earnings. The final amount remaining after these deductions becomes net profit or net income.

Understanding net income calculations helps people avoid financial misunderstandings. Many individuals assume their gross salary equals spendable money leading to unrealistic budgets. Calculating net income accurately provides a clearer understanding of actual financial capacity.

Businesses also depend on accurate net income calculations when evaluating expansion plans investment opportunities and operational efficiency. Investors frequently analyze net profit margins because they reveal how effectively a company controls expenses while generating revenue.

Why Gross Income Matters in Personal Finance

Gross income plays a major role in financial evaluations even though it does not represent actual take-home pay. Lenders landlords and financial institutions often use gross income when assessing creditworthiness because it reflects total earning power before deductions reduce available funds.

Mortgage lenders commonly examine gross monthly income to calculate debt-to-income ratios. This helps determine whether borrowers can reasonably handle monthly mortgage payments alongside existing obligations. Higher gross income often improves approval chances because it signals greater earning capacity.

Job seekers also rely on gross income when comparing career opportunities. Salary offers are almost always presented in gross terms making it easier to compare compensation packages between employers. However understanding deductions remains important because different benefits and tax structures affect actual net earnings.

Gross income is equally valuable for tax planning. Tax brackets and obligations are often based on gross annual earnings before deductions and credits are applied. Knowing gross income helps individuals estimate tax liabilities retirement contributions and potential refund amounts.

Another reason gross income matters involves retirement planning and investment strategies. Financial advisors frequently use gross income percentages when recommending savings targets. For instance retirement experts may advise contributing a certain percentage of gross salary toward long-term investments.

Although gross income does not represent spendable cash it remains a crucial benchmark in financial decision-making. It measures earning potential supports credit evaluations and provides insight into overall financial strength.

Why Net Income Matters in Everyday Life

Net income affects daily life more directly because it determines how much money remains available after mandatory deductions. This figure shapes budgeting decisions savings plans and spending habits. Without understanding net income people may overestimate financial flexibility and struggle to manage expenses.

Most households build monthly budgets around net income because it reflects actual cash flow. Rent payments utility bills transportation costs groceries and entertainment expenses all depend on available take-home pay rather than gross salary figures. Financial stability improves when spending aligns with realistic net earnings.

Net income also influences emergency savings and investment opportunities. People with higher net income can often save more aggressively reduce debt faster and pursue long-term financial goals. Lower net income may require stricter budgeting and expense management to maintain financial balance.

The importance of net income became especially clear during periods of economic uncertainty and inflation. Rising living costs increased pressure on household budgets making it essential for families to monitor actual disposable income carefully. Even workers receiving salary increases sometimes experienced reduced net income due to higher taxes or insurance costs.

For businesses net income determines sustainability and growth potential. Companies with healthy profits can expand operations hire employees and invest in innovation. Businesses with declining net income may face financial difficulties despite strong revenue figures.

Understanding net income helps individuals and businesses make realistic financial choices. It encourages responsible spending accurate budgeting and long-term financial planning.

Net Income vs Gross Income for Businesses

Businesses use both gross income and net income to measure financial performance but each serves a different purpose. Gross income focuses on operational efficiency and revenue generation while net income measures overall profitability after expenses are paid.

Retail companies often analyze gross income to understand product profitability. By subtracting the cost of goods sold from revenue businesses can evaluate pricing strategies and production efficiency. Strong gross income usually indicates effective sales performance and healthy demand for products or services.

Net income provides a deeper understanding of business success because it includes all operating expenses. Administrative salaries rent marketing campaigns taxes utilities and loan payments all affect final profitability. A company with strong sales but excessive operating costs may still report low or negative net income.

Investors pay close attention to net income because it reflects financial stability and growth potential. Public companies often publish quarterly earnings reports highlighting both gross and net income figures. Positive net income signals profitability while declining profits may raise concerns about management effectiveness or market conditions.

Small business owners also rely on these figures for planning and decision-making. Gross income helps track sales trends while net income determines whether the business generates enough profit to support expansion or owner compensation.

The comparison of net income vs gross income is particularly important for startups and growing businesses. New companies may achieve impressive revenue growth but still struggle financially if operating costs remain too high. Balancing revenue generation with expense control is essential for long-term success.

Common Deductions That Reduce Gross Income

Many factors reduce gross income to arrive at net income. Employees often notice these deductions on pay stubs while business owners encounter them in financial statements. Understanding common deductions helps explain why take-home pay differs from total earnings.

Federal income tax is one of the largest deductions for many workers in the United States. Employers withhold taxes based on earnings filing status and information provided on tax forms. State income taxes may also apply depending on location.

Social Security and Medicare taxes further reduce gross pay. These payroll taxes fund government programs and are automatically withheld from employee earnings. Health insurance premiums dental coverage and vision plans may also decrease net income when employers deduct them from paychecks.

Retirement contributions represent another major deduction. Employees contributing to 401(k) plans or other retirement accounts often reduce taxable income while saving for the future. Flexible spending accounts commuter benefits and life insurance premiums can also affect final take-home pay.

Businesses face different types of deductions and expenses. Rent utilities payroll costs advertising expenses software subscriptions and equipment purchases all reduce net profit levels. Tax obligations further decrease remaining earnings.

Understanding deductions helps individuals and businesses manage finances more effectively. Awareness of these reductions improves budgeting accuracy and supports smarter financial planning decisions.

How Taxes Affect Net and Gross Income

Taxes play a central role in the relationship between gross income and net income. Governments calculate tax obligations using earnings information and these payments significantly reduce final take-home pay or business profits.

For employees payroll taxes are automatically withheld from paychecks. Federal income tax rates vary based on income level filing status and tax deductions claimed. State taxes may also apply further reducing net income. Workers earning higher salaries often experience larger tax withholdings because of progressive tax systems.

Self-employed individuals face additional tax responsibilities because they must pay both employee and employer portions of certain payroll taxes. Freelancers and independent contractors often set aside a percentage of gross earnings to cover quarterly tax payments.

Businesses also encounter multiple forms of taxation. Corporate income taxes payroll taxes sales taxes and local business taxes all affect profitability. Effective tax planning can help companies reduce liabilities while remaining compliant with regulations.

Tax deductions and credits can narrow the gap between gross income and net income. Retirement contributions educational expenses healthcare costs and charitable donations sometimes reduce taxable income. Businesses may also deduct operational expenses depreciation and interest payments.

The discussion around net income vs gross income often becomes more important during tax season because people realize how much taxes influence final earnings. Understanding tax obligations allows individuals and businesses to prepare more effectively and avoid financial surprises.

Using Net and Gross Income for Budgeting

Effective budgeting requires understanding both gross income and net income. While gross income reflects earning potential net income determines actual spending capacity. Confusing these figures can lead to unrealistic budgets and financial difficulties.

Most financial experts recommend building budgets around net income because it represents available cash flow. Monthly expenses such as housing groceries transportation insurance and entertainment should align with take-home pay rather than total salary figures.

Gross income still plays a useful role in long-term financial planning. Retirement savings goals investment contributions and debt ratios are often calculated as percentages of gross earnings. Using both figures together creates a more balanced financial strategy.

Budgeting becomes especially important for individuals with fluctuating income such as freelancers or commission-based employees. Tracking average net income helps create more stable spending habits despite income variability. Emergency savings also become critical in these situations because earnings may change monthly.

Businesses also use gross and net income figures for budgeting purposes. Gross income projections help estimate sales performance while net income forecasts determine profitability and cash flow management. Accurate budgeting supports hiring decisions inventory planning and expansion strategies.

People who understand the difference between these figures usually make stronger financial decisions. They are more likely to avoid overspending manage debt responsibly and maintain consistent savings habits over time.

Financial Mistakes People Make With Income Calculations

Many financial mistakes occur because people misunderstand the difference between gross income and net income. One of the most common errors involves budgeting based on gross earnings instead of actual take-home pay. This often leads to overspending and difficulty covering monthly expenses.

Another mistake occurs during job comparisons. Some employees focus entirely on gross salary offers without considering taxes healthcare costs retirement benefits or commuting expenses. A higher salary does not always produce higher net income if deductions and living costs increase significantly.

Freelancers and self-employed workers frequently underestimate tax obligations. Without employer withholding they may spend gross earnings without reserving funds for taxes. This creates financial stress when quarterly or annual tax payments become due.

Businesses can also misinterpret financial performance by focusing too heavily on gross revenue. Strong sales figures may appear impressive but excessive operating costs can still result in low profitability. Business owners who ignore net income trends risk cash flow problems and long-term financial instability.

Loan applicants sometimes overestimate borrowing capacity because lenders evaluate gross income differently from actual spending power. Taking on debt based solely on gross earnings may create repayment difficulties if net income remains limited.

Avoiding these mistakes requires careful financial analysis and realistic planning. Understanding both income figures helps individuals and businesses maintain healthier financial habits and achieve greater stability.

Conclusion

Understanding the difference between net income vs gross income is essential for anyone managing personal or business finances. Although both terms describe earnings they provide very different perspectives on financial health. Gross income measures total earnings before deductions while net income reveals the amount actually available after taxes and expenses are removed.

Gross income helps evaluate earning potential qualify for loans and compare salaries or business revenue performance. Net income however plays a more practical role in daily financial decisions because it determines spendable cash and actual profitability. Together these figures create a complete picture of financial reality.

Individuals who understand these concepts can budget more effectively prepare for taxes accurately and make smarter financial decisions. Businesses that monitor both gross and net income can better control expenses improve profitability and support long-term growth.

The relationship between these figures affects nearly every financial activity from applying for mortgages to managing investments and running successful businesses. Whether you are an employee reviewing paychecks a freelancer handling taxes or an entrepreneur tracking profits understanding these concepts provides greater financial clarity and confidence.

By learning how deductions taxes and expenses influence earnings people gain the tools needed to build stronger financial futures. Knowledge of net income and gross income ultimately supports smarter planning better money management and improved financial stability.

FAQs

What is the main difference between gross income and net income?

Gross income is the total amount earned before taxes and deductions while net income is the amount left after all deductions and expenses are subtracted. Net income represents actual take-home pay or profit.

Why is net income lower than gross income?

Net income is lower because taxes insurance premiums retirement contributions and other deductions reduce total earnings. Businesses also subtract operating expenses and taxes from gross revenue.

Which income figure should I use for budgeting?

Net income is the better choice for budgeting because it reflects the actual money available to spend after deductions. Using gross income can lead to overspending and financial strain.

Do lenders look at gross income or net income?

Most lenders focus primarily on gross income when evaluating loan applications. However they may also consider debt obligations and overall financial stability before approving loans.

Can gross income and net income be the same?

In most cases they are different because deductions and taxes usually apply. However if no deductions or expenses exist gross income and net income could technically be equal.

Why do businesses track both gross and net income?

Businesses use gross income to measure sales performance and production efficiency while net income shows overall profitability after all expenses are paid.

How can I increase my net income?

Increasing net income may involve reducing expenses lowering tax liabilities through deductions improving salary negotiations or increasing business profitability through better cost management.